When lending or borrowing money, most people have various questions they’re unsure of the answers to.

One is “When should I use a loan agreement vs a promissory note?”

While these terms are sometimes used interchangeably, there are differences between a promissory note and a loan agreement, as they are two separate types of contracts.

In this article, we’ll explain everything you need to know to decide which is best for you.

Key takeaways

- A loan agreement is a contract between a borrower and a lender that specifies what each party has agreed to.

- A promissory note is where one party promises, in writing, to pay a set amount to the other according to their agreement.

- While they’re similar, loan agreements and promissory notes are not the same thing.

- You can use PandaDoc’s extensive library of templates to help you create both types of documents.

What’s the difference between a loan agreement and a promissory note?

Let’s look at a promissory note vs loan agreement in simple terms.

Firstly, what are promissory notes? A promissory note is typically used in less formal situations, e.g., when the borrower and lender have a prior relationship and trust one another.

Specifically, the purpose of a promissory note is for circumstances when smaller amounts of money are pledged.

For instance, a relative lends you money for a deposit on a car. This agreement would likely be written as a promissory note rather than a loan.

It’s important to note that promissory notes are unilateral agreements. The party receiving the money (the payee) must repay it according to the contract terms.

However, the lender or payer isn’t legally bound to loan the money in the first place.

Promissory notes specifically deal with unsecured debt.

While the agreement may set forth what happens when a payee defaults, there’s no security for the lender, and they’re likely to have difficulty seeking legal recourse for the money owed.

In contrast, a loan agreement is used for more formal situations and usually deals with large sums of money.

They’re the vehicle of choice for agreements such as mortgages and business loans and are longer and more detailed than promissory notes. As a consequence, they’re also easier to enforce.

Loan agreements are bilateral. Unlike promissory notes, both parties are legally bound to the terms and conditions of the contract and are protected under the agreement.

Regarding security, loan agreements are a form of secured debt. For example, when you buy a car or house, you put the item up as collateral against the loan.

Should you default, the payer can collect the asset and sell it to obtain the money owed.

How are a loan agreement and a promissory note similar?

A loan agreement and a promissory note are financial instruments dealing with money lending. They’re also legally binding.

Both state conditions for the loan and its repayment terms, including a clause stating that the borrower promises to repay the amount set out in the agreement.

Both promissory notes and loan agreements should include the following:

- The principal amount (i.e., the original amount of the loan)

- An agreed-upon interest rate

- Repayment terms, such as a payment schedule and due dates

- What to do in case of default

- The local jurisdiction that the agreement is governed by

- Signatures from both parties (some states may also require a witness or notary to be present)

What is a promissory note?

Let’s look at this in more detail.

A promissory note is a legal “promise” to repay a loan. It’s sometimes known as a note payable, payment on demand or payment on arrival.

The borrowing party promises to repay the loan according to specified terms.

A promissory note is often viewed as a legal IOU. However, strictly speaking, an IOU is a written record of a debt, not a promise to repay this by the borrower.

If you want to learn more, PandaDoc has a handy article on how to write a promissory note to talk you through this process.

What does a promissory note contain?

Promissory notes are simple and concise legal agreements.

They’re straightforward to use and should include essential information such as:

- Details of the parties involved

- The amount loaned to the payee

- The maturity date or final due date of the loan

- The interest rate (as an informal agreement between friends and family, it’s not uncommon for this to be zero)

- Accepted payment methods

- Any late payment fees or other penalties

- Signatures

Use our free promissory note template to make sure you don’t miss anything.

What purpose does a promissory note serve, and when can I use it?

So, what’s a promissory note for? A promissory note is a clear and easy-to-understand document for informal loans.

OK, but how does a promissory note work? It is an intuitive financial instrument for laypeople when procuring or lending money.

It can be drawn up with minimal legal advice compared to a loan agreement.

A promissory note works best in circumstances where all the involved parties know and trust one another.

The following are example use cases for promissory notes:

- Personal loans between friends and family

- Small business or startup loans from private individuals

- Business transactions as a form of short-term credit

- Private financing situations for education or other purchases

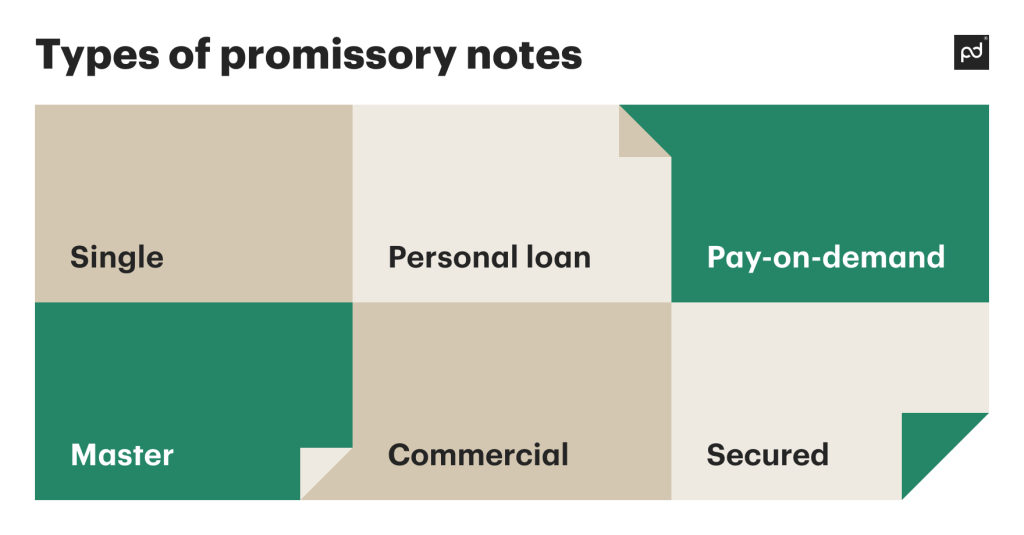

Let’s now look at the various types of promissory notes that exist.

Single promissory notes

This is the most common type of promissory note. Also known as a primary agreement, it outlines the various terms and conditions for loan repayment.

Personal loan promissory notes

An informal or personal promissory note contains terms and conditions to prevent disputes between friends and family.

The inclusion of an interest rate and repayment terms are not mandatory. In most cases, they depend on the relationship between the parties involved.

An informal promissory note’s terms may be more difficult to enforce than those of a loan agreement.

Pay-on-demand promissory notes

A pay-on-demand promissory note differs from the standard agreement type.

In it, the borrower agrees to repay the owed amount as a lump sum rather than in installments. As you might expect, the borrower can “demand” repayment anytime.

Once payment is demanded, the borrower must repay this immediately. So, this type of promissory note is best suited to smaller loan amounts.

Master promissory notes

If you’ve ever taken out a student loan, then you’re already familiar with master promissory notes (MPNs).

An MPN allows the borrower to take out multiple loans, all with the same terms and conditions outlined in the original promissory note.

Commercial promissory notes

This is a type of promissory note issued by banks and credit unions. Borrowers may obtain these for agreements, including auto, personal, or business loans.

Small loans are likely to be unsecured, while more considerable sums may be secured using primary loan agreements.

Secured promissory notes

While not as common as the other types of promissory notes mentioned in this list, payee collateral can also be attached as a form of secured debt.

This provides greater protection for the lender.

Pros and cons of a promissory note

Like any legal agreement, a promissory note has advantages and disadvantages.

Promissory note pros include:

- Simple to write

- Short and easy to understand

- Less/no legal counsel required

- Good for non-traditional lending

- Binds the payee to repay the loaned amount

- Useful for smaller loan amounts

Promissory note cons, on the other hand, include:

- Unsecured debt (this offers less protection to the lender)

- No protection for the borrower, as the lender isn’t legally obligated to do anything

- More likely to result in legal disputes should a problem arise

- Unsuitable for large or complex loans

What is a loan agreement?

Now, onto loan agreements.

A loan agreement is a formal, detailed contract between a borrower and a lender. It covers the terms of the loan and its repayment.

As a multi-page agreement, it sets out conditions such as what will happen in the event of late payments or defaulting on the loan.

Loan agreements are typically secured debts. They’re commonly used for mortgages and car and business loans.

What does a loan agreement include?

Loan agreements span multiple pages and go beyond the basics covered in a promissory note.

They’ll usually include the following:

- The involved parties (details of the borrower and lender, including their names, addresses, and social security numbers)

- The loan principal

- An agreed-upon interest rate

- Loan repayment terms, such as frequency, duration, and due dates

- Collateral

- Methods of payment

- Late fees and other penalties

- What will happen in the event of defaulting on the loan

- Additional provisions, such as “Cure of Default” and indemnification for attorneys

- State laws that apply

- Signatures

As you can probably tell, loan agreements are much more complicated to put together than promissory notes.

With so much to cover, the last thing you want is for them to be held up waiting for individual signatures.

Fortunately, PandaDoc features electronic signature software to keep your document workflows moving.

When is it better to use a loan agreement?

Loan agreements are often more suitable when large sums of money are involved.

They offer more expansive protection for both parties, and debt can easily be secured against collateral.

Let’s consider an example. Say you’re loaning $25,000 to a friend to buy a car.

You’re doing this to help them as you’d like to offer them more advantageous repayment terms than a standard lender.

With a promissory note, you’d have difficulty getting anything back if your friend stopped making repayments.

With a loan agreement, on the other hand, you could legally seize the car and sell it to pay off their debts if the worst happened.

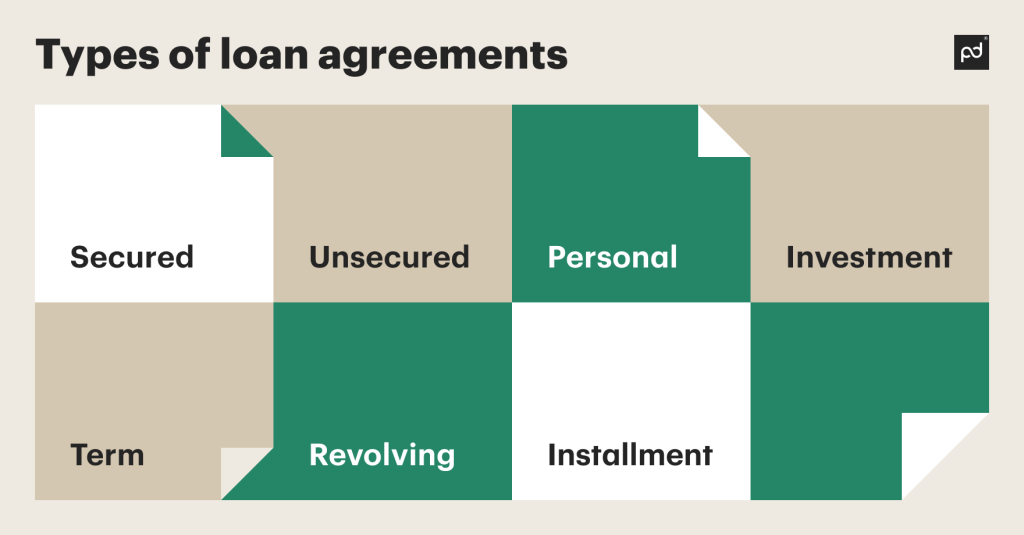

Loan agreements can be tailored to suit any circumstance. Here are some basic loan agreement categories.

Secured loan agreements

As mentioned, most loan agreements are secured by collateral.

Common examples include mortgages and auto and business loans.

Unsecured loan agreements

Going against the grain, an unsecured loan agreement has no collateral.

It’s a form of unsecured debt with limited legal remedies in case of default.

Personal loan agreements

Any loan between two individuals can be drawn up as an official loan agreement.

This allows loans to family, friends, or private individuals to benefit from maximum legal protection—especially when dealing with large sums of money.

Investment loan agreements

An investment loan agreement defines the terms and conditions of a loan taken out for the purpose of investing.

Typically, contract terms set forth how the funds will be used, e.g., for acquiring assets, expanding, or purchasing new equipment.

Notably, an investment loan differs from a convertible note, which is closer to an IOU (with interest) and can be paid off with equity instead of cash.

Term loan agreements

A term loan agreement is a very common loan type.

The borrower is provided with a lump sum upfront and agrees to repay this over a specified period. Interest may be fixed or variable and will affect how long the loan takes to pay off.

Revolving loan agreements

Unlike a term loan, a revolving loan provides a line of credit instead of cash. It offers flexible terms for repayment and borrowing additional sums.

Like a term loan, it stipulates whether interest is variable or fixed.

Revolving loan agreements are the basis for most consumer credit accounts and overdrafts.

Installment loan agreements

An installment loan agreement is similar to a term loan agreement. Typically, the payee makes fixed payments until the loan is repaid.

This type of loan is attractive to borrowers as it usually garners lower fixed interest rates.

If you need help drafting a loan agreement, why not use our free loan agreement template to guide you through the process?

Pros and cons of a loan agreement

Like promissory notes, loan agreements also have their pros and cons.

Benefits include:

- Ease of attaching payee collateral

- Good for secured debt

- Offer maximum protection for the lender

- Legally binding for both the lender and borrower

- More suitable than promissory notes for lending large amounts of money

- Lots of flexibility regarding loan and repayment terms

Loan agreement cons include:

- Complex to write

- Legal advice is needed

- Take longer to draw up and implement than promissory notes

- Not as easy to use for re-borrowing

- Less suited to smaller loans

Do I need both a promissory note and a loan agreement?

In most cases, only one of these will be necessary.

Promissory notes are more suited to smaller, informal, and unsecured lending, whereas loan agreements are better for complicated situations involving more significant sums of money.

However, occasionally, lenders and borrowers may wish to include both a promissory note and a loan agreement.

That’s because using both financial instruments can bring greater clarity to complex lending situations.

A common example is student loans.

In this instance, payees sign a multi-page loan agreement that outlines broad terms and conditions.

Additionally, a secondary master promissory note outlines simple terms for repayment and re-borrowing. This streamlines the process of funding education and its variable costs.

Create a loan agreement or promissory note with effective and easy-to-use PandaDoc software

Lending and borrowing money is stressful enough on its own — you don’t want to be weighed down by legalese, jurisdictions, and exorbitant legal fees on top of this.

That’s why you should use document management software from PandaDoc.

Our solution helps generate legal documents and contracts with ease and can get you up and running with loan agreements, promissory notes, and other important documents in no time.

Sign up to PandaDoc today and take the pain out of document management!

Disclaimer

PandaDoc is not a law firm, or a substitute for an attorney or law firm. This page is not intended to and does not provide legal advice. Should you have legal questions on the validity of e-signatures or digital signatures and the enforceability thereof, please consult with an attorney or law firm. Use of PandaDocs services are governed by our Terms of Use and Privacy Policy.