When it comes to real estate loans, lenders and borrowers take on a lot of responsibility — and risk. Acceleration clauses can help manage these issues.

In this comprehensive guide, we’ll discuss the definition of an acceleration clause, what triggers it, and how it might affect you.

Key takeaways

- Most mortgage agreements contain acceleration clauses, so it’s important to understand them and how they work.

- Acceleration clauses can have several triggers that should be clearly outlined in the loan contract.

- The result of triggering an acceleration clause is often foreclosure.

- It’s best practice for lenders and borrowers to avoid triggering an acceleration clause.

What is an acceleration clause?

An acceleration clause is a provision in a contract that allows a real estate lender to demand immediate repayment of the entire outstanding balance if the borrower fails to meet certain conditions or obligations.

The lender can also demand any interest incurred since the last repayment.

The clause provides lenders with a safeguard against default. Almost every mortgage contains one, and the clause includes several terms the borrower must meet to maintain the loan.

If the borrower fails to fulfill these terms, the lender can trigger the acceleration clause.

Once a mortgage acceleration clause is triggered, the borrower must repay the outstanding balance in full.

If the balance cannot be repaid, the borrower risks their property being entered into foreclosure.

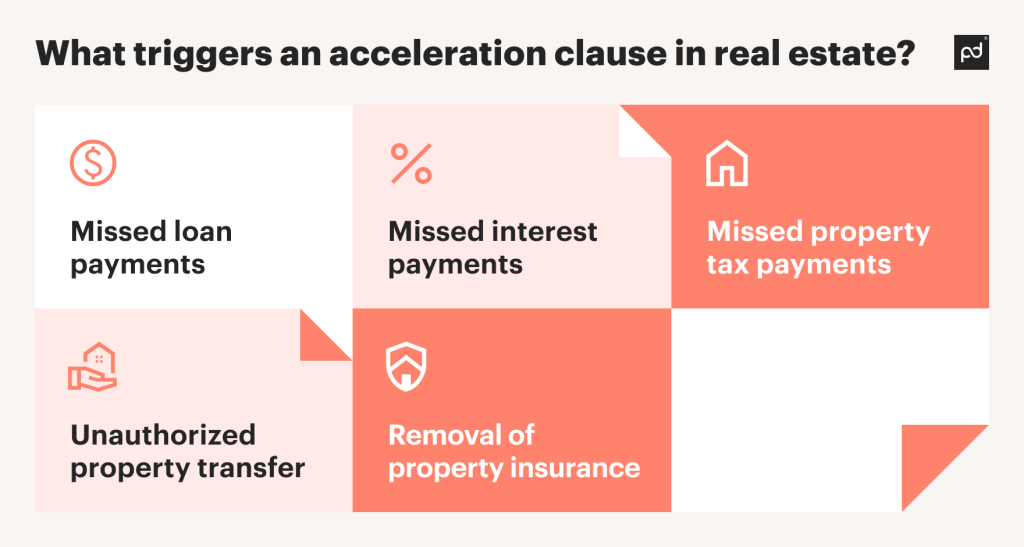

What triggers an acceleration clause in real estate?

Lenders can trigger an acceleration clause for a variety of reasons. Let’s look at a few.

Missed loan payments

This is the most common trigger.

The number of missed repayments will vary depending on the contract, but once a borrower has hit that number, the lender can trigger the acceleration clause.

Missed interest payments

Similar to missed loan payments, a certain amount of missed interest payments can result in an acceleration clause trigger.

Missed property tax payments

Unpaid property taxes can result in a tax lien on a property. This allows the local government to claim it should the owner regularly fail to pay property tax.

After several missed payments, the local authority can seize the property to recoup their losses.

Tax liens often trump mortgage agreements since they’re directed by the Government.

This puts lenders at risk of losing out, so many loan contracts include missed property taxes as an acceleration clause trigger.

Unauthorized property transfer

If a property owner/borrower wishes to transfer ownership to another, the financial lender must know that the new owner is trustworthy, reliable, and can afford the mortgage repayments.

Any transfers must therefore be thoroughly checked and authorized by the lender. If a borrower makes an unauthorized transfer, the lender can usually trigger a mortgage acceleration clause.

Removal of property insurance

Many mortgage agreements require the borrower to have insurance to maintain and protect the property properly.

An acceleration clause can be triggered by the removal of this insurance.

What factors do lenders consider when deciding whether to accelerate?

Accelerating a loan tends to be a last resort on behalf of the lender, so triggering this extreme contract clause is rarely cut and shut.

There are certain factors that lenders must consider when deciding whether to do so.

- If missed loan payments or a temporary financial hardship caused lapsed property insurance, the borrower might be able to get things back on track—and most lenders will try to facilitate this opportunity.

- Lenders must ensure that their contract clearly defines the acceleration clause, its triggers, and its consequences before trying to enforce it.

- If the borrower is communicative and open to remediation, lenders might be able to negotiate a less extreme solution (and should be open to trying).

- However, if the lender gets stonewalled at every turn, triggering acceleration might be the only option.

What is a notice of intent to accelerate?

A notice of intent to accelerate (NOIA) is a legal document spelling out the lender’s intent to accelerate the loan.

If the borrower breaks the terms of their loan agreement, the lender must send an official notice informing them of:

- Which terms they broke

- The steps the borrower must take to rectify the issue

- The timeframe the borrower has to comply

- Further action the lender intends to take should the borrower fail, i.e., accelerating the loan

What happens when a loan is accelerated?

When a loan is accelerated, the lender can demand full repayment of the outstanding balance plus any interest accrued.

If the borrower cannot repay the loan fully, they’ll likely be subject to property foreclosure.

However, there are certain steps that both borrowers and lenders can take between a notice of intent to accelerate and foreclosure. We’ll look at these in a bit.

Acceleration clause example

Here’s an example from the SEC to give you an idea of what a mortgage acceleration clause might look like.

15. Remedies.

(a) Acceleration of Maturity. If an Event of Default shall have occurred, then the entire Indebtedness shall, at the option of Lender, immediately become due and payable without notice or demand, time being of the essence of this Security Instrument, and no omission on the part of Lender to exercise such option when entitled to do so shall be construed as a waiver of such right.

Here, “Event of Default” means any triggers the lender has set for the acceleration clause.

How to avoid an acceleration clause being used

It’s always best to avoid disaster where possible.

Triggering a mortgage acceleration clause can put a huge amount of stress on both lenders and borrowers, leading to financial losses, legal costs, property foreclosure, and damage to the borrower’s credit score.

So, how can all this be avoided?

- Both parties should consider the terms of the loan agreement carefully before entering to avoid a contract dispute. Borrowers must ensure they can uphold any requirements and lenders must do due diligence into anyone they lend money to.

- If a borrower finds themselves in financial hardship and unable to make repayments, they should contact their lender immediately to discuss options. It’s better to be upfront than hit with a NOIA down the line.

-

Options are subject to the lender and include:

- Forbearance. Lenders can reduce or halt loan payments for borrowers going through temporary financial hardships.

- Loan modification. Lenders can modify the terms to reduce monthly payments.

- Refinancing. Refinancing for a better mortgage is sometimes an option for those with equity on their property, although it can be difficult for borrowers already in default to secure.

- Asking for mortgage assistance. Getting advice and help from professionals can ease the burden on borrowers.

- If a NOIA is delivered, the borrower should contact their lender and explain their situation.

- As difficult as the situation is, it helps if borrowers and lenders can be empathetic and open to discussion.

Options after acceleration

Once a lender has triggered a contract penalty clause, options become more limited. They include:

Foreclosure

We’ll start with the big one. Foreclosure is when the lender seizes property ownership and sells it to recoup their losses.

It’s the worst-case scenario, and there are still options to avoid it post-acceleration.

Right to reinstate

To avoid foreclosures, many states have laws that allow borrowers to reinstate their mortgages, provided they can make up for all missed payments and cover any costs the lender incurred enforcing the contract.

Even in states without this law, many lenders include a right to reinstate their loan agreements.

Repayment plans

Very few borrowers in default can repay a large loan in full. So, lenders may sometimes arrange a repayment plan to alleviate this burden.

Selling

If the outstanding balance is less than the property value, selling can be a good option.

Short sales

If the outstanding balance exceeds the property value, some lenders will let the borrower sell their home and accept a smaller amount to settle the loan.

This will nonetheless impact the borrower’s credit score.

Deed in lieu of foreclosure

Borrowers can also transfer the property deed to the lender in lieu of foreclosure, which can avoid damaging the borrower’s credit score.

Simplify all your real estate business with robust automation software

Acceleration clauses are just one thing real estate businesses have to deal with.

Juggling the writing, access, tracking, compliance, storage, and sharing of legal documents can also drain time and resources that are better spent elsewhere.

Luckily, PandaDoc offers a comprehensive document management solution for real estate businesses looking to organize and streamline their operations.

Why not sign up for a free 14-day trial today?

Disclaimer

PandaDoc is not a law firm, or a substitute for an attorney or law firm. This page is not intended to and does not provide legal advice. Should you have legal questions on the validity of e-signatures or digital signatures and the enforceability thereof, please consult with an attorney or law firm. Use of PandaDoc services are governed by our Terms of Use and Privacy Policy.

Frequently asked questions

-

In short, yes.

Once both parties have signed a loan agreement, the terms are binding. Lenders seizing assets and subjecting borrowers to foreclosure can be traumatic, but it’s nonetheless legal.

As with all legal documents, however, it’s important to check that the terms are fair, enforceable, worded correctly, and understood by all parties before signing.

Any problems with a contract can lead to questions surrounding its legality.

-

An alienation clause (or due-on-sale clause) is another type of clause that can trigger the total repayment of an outstanding loan balance.

Unlike a mortgage acceleration clause, triggered when a borrower fails to uphold their responsibilities, an alienation clause triggers during a sale.

If a borrower decides to sell their home while still under their mortgage contract, an alienation clause ensures the outstanding loan balance is paid back to the lender from the proceeds.